Catalysis refers to the acceleration of a chemical reaction caused by the presence of a substance known as a catalyst. A catalyst is not consumed during the reaction and remains unchanged after the reaction is complete. If the reaction proceeds quickly and the catalyst is regenerated efficiently, even small amounts of the catalyst can be effective. Factors such as mixing, surface area and temperature play a significant role in determining the reaction rate. Catalysts typically interact with one or more reactants to form intermediates, which then produce the final reaction product and simultaneously regenerate the catalyst. The recent increase in volatility in the stock and currency markets can be attributed to a catalyst. This catalyst has been identified as the simultaneous occurrence of several economic events, each driven by its own catalyst. Now we will examine the three main components of this catalyst: 1. the unwinding of the yen carry trade; 2. leading US economic indicators pointing to an impending recession; and finally 3. disappointing earnings from megacap companies. The combination of these factors accelerated the market reaction and provided investors with compelling reasons to take profits quickly. Let’s take a closer look at each of these elements.

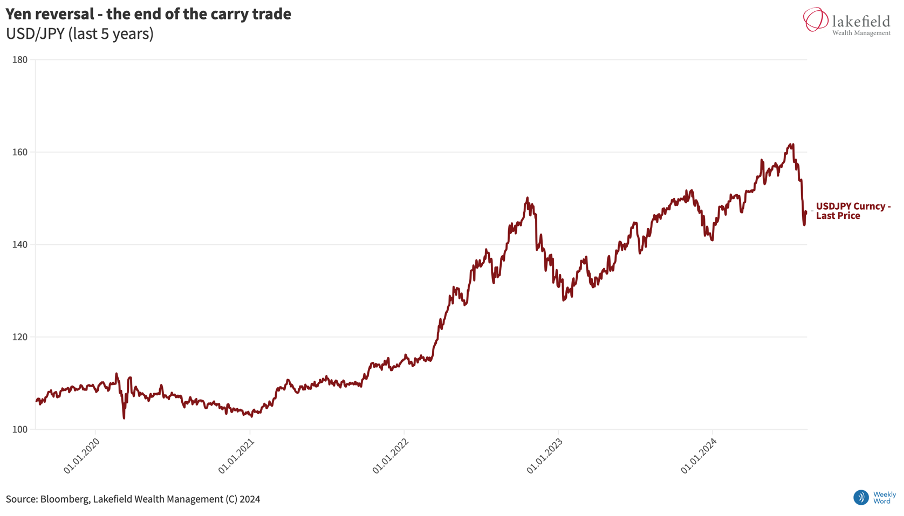

The recent crash of the Japanese stock market and its impact on Western markets was largely caused by a sudden reversal of the Japanese yen. For years, investors around the world have taken advantage of low interest rates in Japan by borrowing cheaply in yen to invest in foreign assets, including large US technology stocks – a strategy known as the “yen carry trade”. This reversal was economically driven. After years of deflation, Japan finally entered a positive inflationary environment, prompting the Bank of Japan to raise interest rates. Although this move was expected, the markets were surprised by the announcement that this was only the first of many rate hikes. This not only led to a sharp rise in yen borrowing costs, but more importantly to a rapid and significant appreciation of the yen. In order to avoid losses and margin calls, investors were forced to liquidate their positions quickly, resulting in the liquidation of an estimated 4 trillion dollars in assets in just a few days.

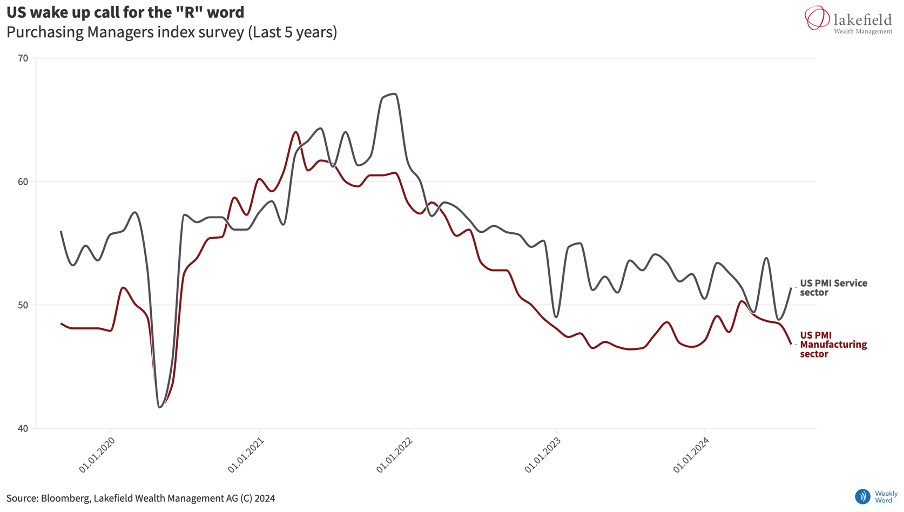

In addition, two economic reports at the beginning of August – a survey on the manufacturing industry and official labor market data – reinforced fears that the US economy was heading for a recession. Concerns grew that the Federal Reserve was making a mistake by not lowering interest rates quickly enough. Previously, investors had been relatively reassured by the prospect of a soft landing for the US economy. However, the unexpectedly weak data shook this confidence and fueled speculation of an emergency rate cut. This led to a rally in bonds and a fall in the US dollar.

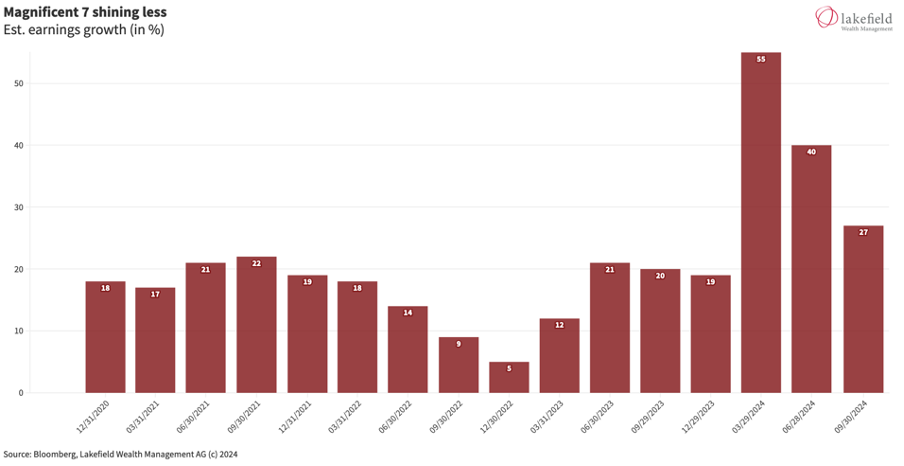

In addition, the current reporting season has not delivered the positive surprises that were seen in previous quarters. In combination with excessive valuations for mega-cap companies, this has led to rapid profit-taking. The situation was exacerbated by Warren Buffett’s announcement that he had further reduced his position in Apple shares.

Each of these factors could possibly have been overcome on its own.

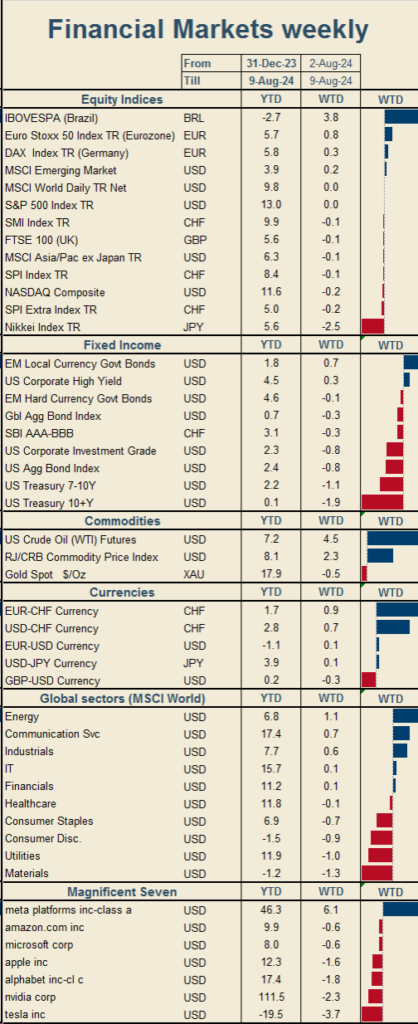

However, their simultaneous occurrence created a strong catalyst that had a significant impact on the markets. Looking ahead, volatility is expected to normalize, but several upcoming events could keep volatility high compared to previous levels. The coming weeks will provide more data for the Federal Reserve and investors to navigate the future. Of note, bonds have begun to decouple from stocks, suggesting that upcoming rate cuts may not be for favorable reasons.

The Japanese yen has experienced an almost continuous decline since 2021, largely due to the widening interest rate differential between Japanese and US bonds. For Japan’s export-oriented economy, a weaker yen generally supports economic growth. However, the yen’s sudden 8.5% rise against the US dollar from July 31 to August 5 led to an accelerated reversal of the carry trade. The unwinding of yen carry trades could be reflected in short-term fluctuations in the yen. A lower yen typically indicates more stable market conditions.

Recent leading economic indicators, in particular the Purchasing Managers’ Index (PMI), point to worrying trends. The manufacturing PMI fell well short of expectations, coming in at 46.8 compared to the expected 48.8. A reading below 50 indicates a decline. Although the US is not currently in recession and GDP growth forecasts are 2.1% for the third quarter and 1.6% for the fourth quarter, a slowdown is evident, even if a contraction has not yet occurred. Particular attention should be paid to unemployment trends, as an increase in unemployment could have a negative impact on consumer financing and lead to more profound economic challenges.

The recent strong performers of the S&P 500, known as the “Magnificent Seven”, have shown slower growth prospects in recent quarters. With a price/earnings ratio of 34, a slowdown in growth is a direct reason for profit-taking.

.

Disclaimer: This document has been prepared by Lakefield Wealth Management AG with care and to the best of its knowledge and belief. However, Lakefield Wealth Management AG assumes no responsibility for the accuracy and completeness of the content and disclaims any liability for losses that may arise from the use of this information. The information presented here is for information purposes only and is intended solely for the intended recipient. Reproduction, redistribution or republication of this document for any purpose is strictly prohibited without the prior written permission of Lakefield Wealth Management AG. The content of this document should not be interpreted as a solicitation or offer to buy or sell securities, related financial instruments or to engage in any other transactions. It should be noted that the information in this document is not intended as investment, legal or tax advice. This document is not directed at US persons (as defined in Regulation S under the US Securities Act of 1933, as amended) or any person in any jurisdiction where access to or publication of this document is prohibited by reason of that person’s nationality, residence or otherwise. Access to this document is prohibited for persons subject to local restrictions. Every investment involves inherent risks, particularly with regard to fluctuations in value and returns. Investments in foreign currencies entail additional risks, as the foreign currency may depreciate against the investor’s reference currency. Historical returns should be understood as indicative and do not guarantee future performance. Furthermore, there is no guarantee that the performance of the reference index or benchmark will be matched or exceeded. Furthermore, the information provided herein does not take into account the specific or future

Source: Bloomberg, Lakefield Wealth Management AG, © 2024