Officials at the European Central Bank (ECB), led by President Christine Lagarde, have cut the key interest rate for deposits by a quarter of a percentage point to 3.75%. This decision follows a significant improvement in the inflation outlook. However, the ECB plans to maintain the restrictive interest rates for as long as necessary. The rate cut, described as “hawkish easing”, required an agreement to raise inflation expectations in order to secure approval for the move. The timing of the ECB’s next measure remains uncertain. With the disinflation process firmly underway, the ECB, along with other central banks, is expected to gain more confidence in easing monetary policy further. This rate cut is significant for the ECB as it is the first time in two decades that policymakers have embarked on a cycle of monetary easing without being forced to do so by a financial emergency. Instead, investor confidence in the eurozone is ensuring stable yields.

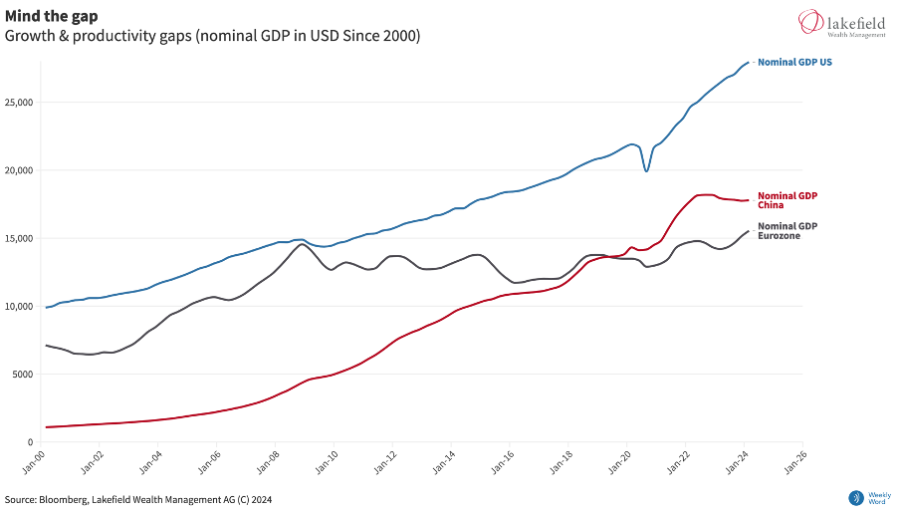

Despite a seemingly calm surface, underlying economic problems that have built up over decades are becoming increasingly visible. The eurozone continues to struggle with sluggish growth, weak productivity, unfavorable demographic trends and high public debt in key countries. This period of stable markets and economic recovery provides a rare opportunity for Brussels and national governments to address these challenges. However, with the upcoming European elections, there is a risk that politicians will not seize this opportunity to implement growth-enhancing reforms and improve public finances, which could lead to a further decline in the region’s global importance. The Eurozone urgently needs to reindustrialize to keep pace with the US and emerging markets. Without significant and bold policy action, the European Union risks reducing its global influence, which will see the US and China competing for economic supremacy. Weak productivity and low growth potential remain key issues that need to be addressed for long-term stability and prosperity. Since the beginning of the 21st century, the EU has consistently underperformed the US in these areas. Slower improvements in living standards and a decline in global economic strength are the consequences. According to Bloomberg Economics, the gap between the European and US economies since 2000 reached around 18% of potential GDP in 2023, equivalent to more than €3 trillion, with projections suggesting that the deficit could reach almost 40% by 2050. The eurozone is currently at a crucial juncture. The ECB’s interest rate cut coincides with the end of the worst inflationary phase in the currency’s history and a surprising growth spurt following a shallow recession. The spread between Italian and German bonds, a key measure of risk, narrowed to a two-year low in early 2024. Although yields have risen slightly as investors reassess the ECB’s ability to cut rates further given the resilient economy, there is no sign of the fragmentation fears that worried the market ahead of the first rate hike in 2022.The Eurozone policy environment has become more coherent and now includes the European Union’s unprecedented pandemic-induced recovery program, NextGenEU. This initiative includes joint borrowing and new crisis-fighting instruments introduced by the ECB to provide stimulus and stabilize bond markets. Despite recent improvements, profound structural challenges remain, including ageing populations, overregulation, climate change and global fragmentation. Contrary to expectations, the “cut” signaling the end of an action must be seen as the beginning of bolder measures.

For more than two decades, the US has been in a growth phase that is not only more stable but also steeper than Europe and China. This is due to the increase in productivity in the US. It is currently believed that AI could give this growth an additional boost. Whether this boost will come from American companies or their applications remains to be seen. What is clear, however, is that Europe must quickly reorient itself in order to keep public debt sustainable.