As we write, the US is counting the 150 million or so votes to determine the outcome of the 60th quadrennial presidential election. At the moment, Trump is in the lead, but the vote count continues and the final result will not be announced until later. Historically, financial markets tend to react more strongly to long-term economic developments and fundamental trends than to political leaders. Political decisions and changes of government can generate short-term fluctuations and momentum, but in the end it is primarily economic factors such as growth, inflation and interest rate policy that shape the course of the markets. The US presidential elections in 2024 will therefore focus less on the names of the candidates and more on the question of which economic policy strategies can secure long-term stability and growth for the USA. Because investors know: It is the economic conditions, not necessarily the policies, that give the stock markets a long-term boost. The real focus of the markets is therefore not on which candidate is seen as more “stock market friendly” in the short term, but on who will provide the most sustainable support for the economy.

De presidentsverkiezingen van 2024 brengen twee duidelijk omlijnde scenario’s met zich mee die zouden kunnen leiden tot verschillende economische vooruitzichten en reacties voor de markten. Een mogelijke herverkiezing van Trump, samen met een Republikeinse meerderheid in het Congres (“red sweep”), zou belangrijke economische gevolgen kunnen hebben, aangezien een dergelijke meerderheid voorstander zou kunnen zijn van deregulerende en groeibevorderende maatregelen. Een presidentschap van Harris zou daarentegen kunnen leiden tot een strakker gecontroleerd fiscaal beleid en lagere uitgaven. De potentiële impact van elk scenario op de belangrijkste sectoren en markten wordt hieronder geanalyseerd.

Government bonds and interest rates: A steeper yield curve is expected under a Trump administration with a “red sweep”. Increased government debt and a looser fiscal policy stance could weigh on the bond market and drive up yields, which in turn leads to inflation expectations. ING assumes that the 10-year yield could rise to up to 5 %. In contrast, more restrictive fiscal measures under Harris would mitigate the rise in yields.

Equities and volatility: A “red sweep” could boost the stock market in the final months of the year. Deregulation measures and a growth-oriented agenda are likely to support banks, energy companies and the transportation industry in particular. This could trigger a market rotation from safety-oriented investments to riskier stocks. Under Harris, on the other hand, the price trend would be more moderate, as the markets could adjust to stable, albeit less expansive fiscal policy measures.

US dollar and currency markets: A Trump victory is likely to strengthen the dollar, especially if his protectionist measures are extended. Higher tariffs could affect exports to countries such as China, but also weigh on currencies such as the euro, Australian dollar and Mexican peso. In the event of a “red sweep”, the currency markets would record a USD appreciation of up to 7%. Under Harris, on the other hand, the dollar could tend to weaken as a result of more moderate trade and more stable international policy.

Energy and commodities: Trump’s energy independence agenda could lead to a short-term rise in oil prices. In the long term, however, the oversupply that he is seeking to achieve through increased production within the US could put pressure on prices. If Harris wins the election, on the other hand, prices are expected to stabilize or fall slightly due to more restrictive oil production measures and a stronger focus on renewable energies.

Technology and industrials: In a second Trump administration, M&A activity in the technology sector could increase as the focus is on a less interventionist Federal Trade Commission (FTC). Technology stocks that benefit from higher tariffs and manufacturing relocations could outperform other hardware manufacturers as reliance on Chinese imports has decreased. Harris, on the other hand, could support the technology sector through increased support for sustainable technologies and tax incentives for renewable energy.

Healthcare and consumer sectors: Potential M&A activity is on the table for the healthcare sector, though sweeping changes to the Affordable Care Act (ACA) are unlikely. Republicans could seek lower subsidies and less regulation, but without far-reaching changes to the healthcare market. The consumer sector, particularly retail, could also be affected by tariff increases under Trump, while car manufacturers could benefit from stronger trade barriers.

Macro-economische effecten en inflatie: Het economische beleid van een Republikeinse president Trump zou een inflatoir effect kunnen hebben. Het losse fiscale beleid, in combinatie met protectionistische tarieven, zou de inflatie waarschijnlijk doen toenemen en de Fed weinig speelruimte laten om de rente te verlagen. Goldman Sachs Bank ziet daarentegen een gematigdere economische groei, maar een rustiger inflatieklimaat.

In summary, the possible scenarios are each characterized by different economic dynamics. While a Trump administration with a Republican congressional majority will aim for pro-cyclical growth and deregulation, fiscal policy under Harris is likely to aim for stable but more moderate growth. The election will therefore play a central role, but will not influence long-term fundamental market forces.

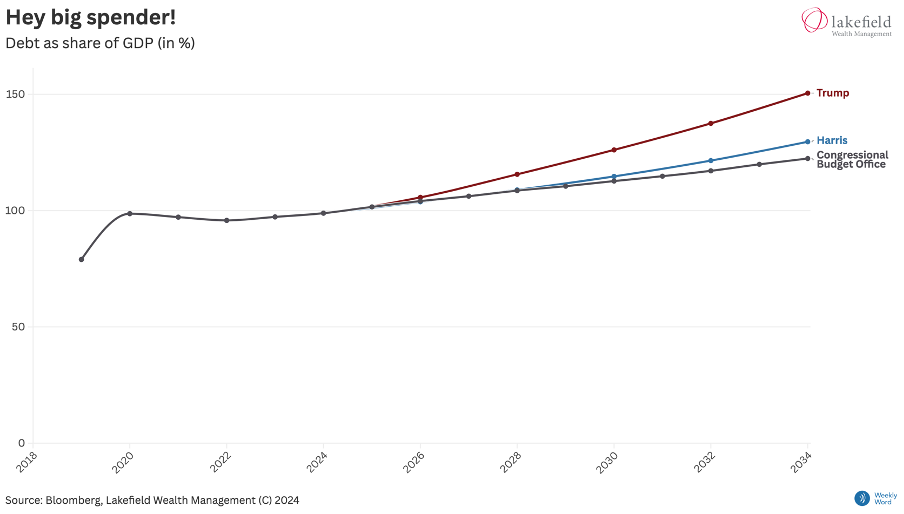

In 2024 zal de VS naar verwachting een begrotingstekort hebben van ongeveer 6,5% en zal de verhouding tussen de overheidsschuld en het bbp stijgen tot bijna 100%, vergeleken met 79% in 2019. Tegen deze achtergrond is het opvallend dat het belastingbeleid van Trump de schuldenlast aanzienlijk zou verhogen, terwijl het beleid van Harris niets zou doen om deze te verlagen.

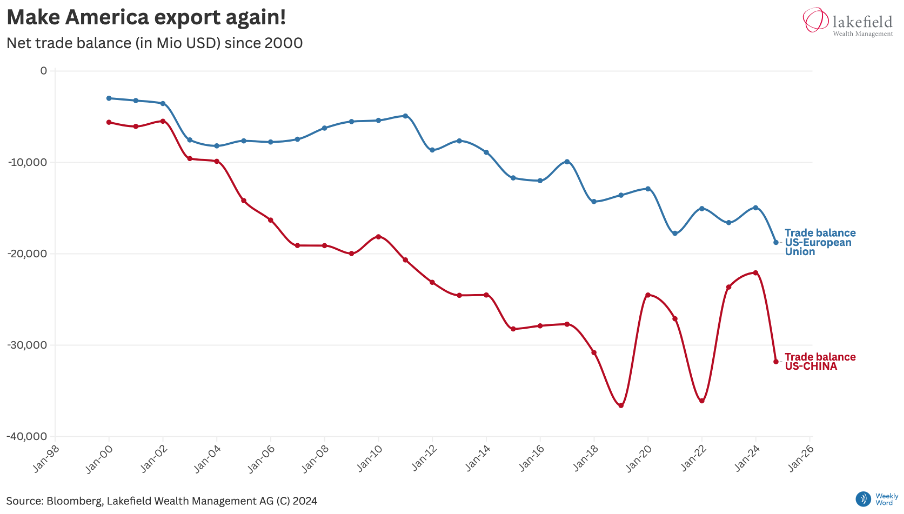

Trump announces new tariffs (10% on all imports + up to 60% on imports from China), while Harris does not plan to increase tariffs. Given the trade deficit the US has built up with China and Europe, the implementation of such a measure will have a significant impact on inflation, interest rates, bonds and profit margins. The least exposure is likely to be found in consumer goods stocks in the services sector such as hotels, restaurants and airlines. This could pose a problem for industrial stocks whose supply chains are focused on China. A shift to friendlier countries is possible. The impact on global trade remains to be seen.

| Harris favorable sectors | Trump favorable sectors |

| Consumer goods | Finance |

| Industry | Communication |

| IT | Consumer goods (discretionary) |

| Green energy | Healthcare |

| Consumer goods (discretionary) | Oil |

| Real estate | Real estate |

.

Disclaimer: This document has been prepared by Lakefield Wealth Management AG with care and to the best of its knowledge and belief. However, Lakefield Wealth Management AG assumes no responsibility for the accuracy and completeness of the content and disclaims any liability for losses that may arise from the use of this information. The information presented here is for information purposes only and is intended solely for the intended recipient. Reproduction, redistribution or republication of this document for any purpose is strictly prohibited without the prior written permission of Lakefield Wealth Management AG. The content of this document should not be interpreted as a solicitation or offer to buy or sell securities, related financial instruments or to engage in any other transactions. It should be noted that the information in this document is not intended as investment, legal or tax advice. This document is not directed at US persons (as defined in Regulation S under the US Securities Act of 1933, as amended) or any person in any jurisdiction where access to or publication of this document is prohibited by reason of that person’s nationality, residence or otherwise. Access to this document is prohibited for persons subject to local restrictions. Every investment involves inherent risks, particularly with regard to fluctuations in value and returns. Investments in foreign currencies entail additional risks, as the foreign currency may depreciate against the investor’s reference currency. Historical returns should be understood as indicative and do not guarantee future performance. Furthermore, there is no guarantee that the performance of the reference index or benchmark will be matched or exceeded. Furthermore, the information provided herein does not take into account the specific or future

Source: Bloomberg, Lakefield Wealth Management AG, © 2024