In the financial markets, the economy usually has the greatest influence. But rarely can politics have a significant impact. This became clear when Liz Truss implemented tax changes in the UK, which had an immediate impact on interest rates, sterling and stock markets. Another notable example is the Greek crisis in the summer of 2011, which posed an existential threat to Europe. Recent elections in Europe have shaken up the ruling parties, with a clear shift towards right-wing parties. In France, around 50% of the vote in the EU elections went to far-right and far-left parties, prompting President Emmanuel Macron to announce an early general election. Markets usually react negatively to political uncertainty. Macron’s decision has introduced a month of unpredictability for traders. His move is aimed at regaining political control after his party suffered a significant defeat to Marine Le Pen’s far-right National Assembly in the European elections. However, many MPs and officials believe that this risky strategy could further weaken his party and hinder his economic agenda, with even the possibility of strengthening Le Pen’s influence.

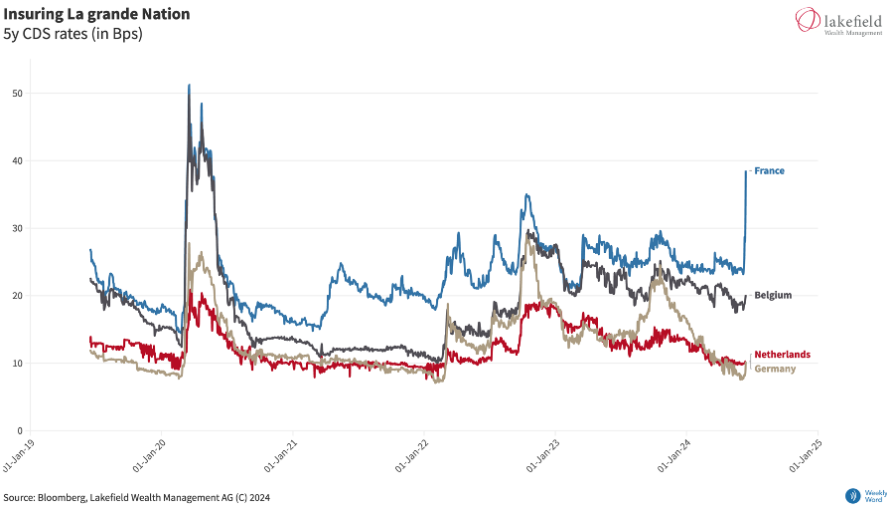

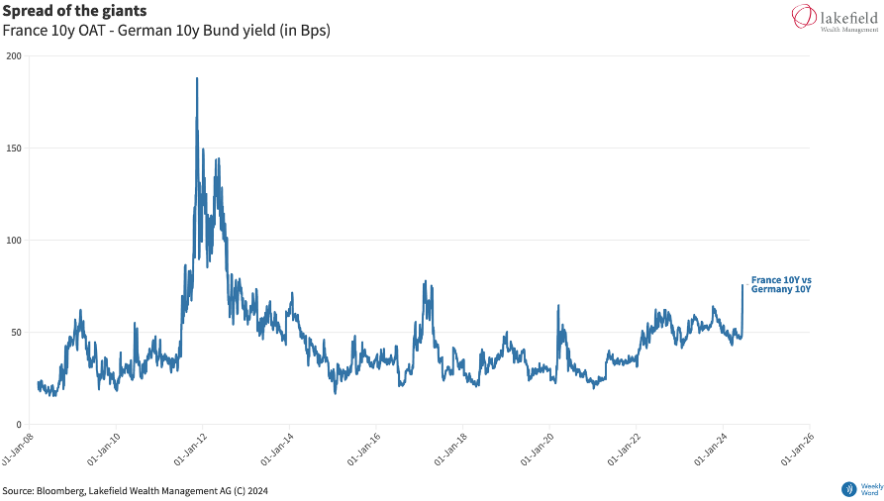

The risk of political instability triggered fears on the bond markets on Tuesday, reinforced by reports that the president had considered resigning if the election results were unfavorable. Markets had not anticipated such a high political risk event in France and Europe, making the current situation particularly significant. To cope with the fallout, President Macron assured in an interview with Figaro Magazine that the election results would not affect his position. Nevertheless, the risk premium on French bonds compared to German Bunds widened to its highest level since the early days of the pandemic in March 2020. The yield on ten-year French bonds rose by up to 10 basis points, widening the spread to the corresponding German bonds to its highest level since March 2020.

The uncertainty also prompted investors to reduce their equity exposure to Italy and Spain, resulting in benchmarks in these countries falling by around 2%. Italian bonds, considered some of the riskiest in the region due to the government’s debt burden, were also affected for the second day, with the spread to Bunds widening to 150 basis points. According to an Ifop poll released on Tuesday, Le Pen’s party is leading in the polls for the first round of elections with 35%, while Macron’s party is 17 points behind, which is in line with EU election results. Parliamentary elections in France are highly unpredictable due to negotiations between the first and second rounds in 577 constituencies.

French stocks suffered their biggest two-day drop in a year as bank shares fell along with the country’s bonds, exacerbating the impact of President Macron’s decision to call an early election. The French election, which will be held in two rounds and conclude on July 7, confronts investors with the risk that Marine Le Pen’s far-right National Assembly could gain control of the legislature. The situation remains extremely volatile, especially in a country with one of the highest levels of public debt.

The premium for hedging French government bonds rose to its highest level since the pandemic last week. Neighboring countries have not yet reacted to this development. While the financial markets are currently looking at the situation in isolation, there is a possibility of contagion that could affect the euro and other countries with similar economic conditions to France

The spread between the yields on ten-year French and German bonds widened last week to a level not seen since 2017. This rise in interest rates on France’s considerable sovereign debt could quickly escalate the situation to undesirable levels.

Disclaimer: This document has been prepared by Lakefield Wealth Management AG with care and to the best of its knowledge and belief. However, Lakefield Wealth Management AG assumes no responsibility for the accuracy and completeness of the content and disclaims any liability for losses that may arise from the use of this information. The information presented here is for information purposes only and is intended solely for the intended recipient. Reproduction, redistribution or republication of this document for any purpose is strictly prohibited without the prior written permission of Lakefield Wealth Management AG. The content of this document should not be interpreted as a solicitation or offer to buy or sell securities, related financial instruments or to engage in any other transactions. It should be noted that the information in this document is not intended as investment, legal or tax advice. This document is not directed at US persons (as defined in Regulation S under the US Securities Act of 1933, as amended) or any person in any jurisdiction where access to or publication of this document is prohibited by reason of that person’s nationality, residence or otherwise. Access to this document is prohibited for persons subject to local restrictions. Every investment involves inherent risks, particularly with regard to fluctuations in value and returns. Investments in foreign currencies entail additional risks, as the foreign currency may depreciate against the investor’s reference currency. Historical returns should be understood as indicative and do not guarantee future performance. Furthermore, there is no guarantee that the performance of the reference index or benchmark will be matched or exceeded. Furthermore, the information provided herein does not take into account the specific or future